The ten-year crisis today we are most worried about: debt problems

Author: Zhang Yuan Dongxing Securities 601,198 bank, clinic chief economist shares

Since the 1970s, there have been financial crises with global influences in every decade: the 1950s was the complete collapse of the Brinton forest system, the 1980s was the Latin American debt crisis, and the 1990s was the Asian financial crisis. The 1990s was the US subprime mortgage crisis. This decade, looking around, there are no signs of a crisis, but we have become a big problem. The debt problem is considered to be one of the main gray rhinoceros in the financial sector. There is little disagreement among the parties. The difference is that it is not clear whether the gray rhinoceros is currently swaying in the grasslands, or has accumulated kinetic energy to come straight to us.

First, the nature of the problem

The fundamental reason for the formation of debt gray rhinoceros is that China has promoted industrialization and urbanization at a high speed in the past few years. As the process of intermediate industrialization draws to a close, the urbanization process enters the second half of the period, and the huge assets formed in related fields may not be depreciated normally. Interest payments, the debt chain may be difficult to maintain.

In an economy like China, the normal industrialization of urbanization may last for 50 years. In the long years, the state and the people have accumulated physical capital, monetary wealth, human resources, and management capabilities, and have invested in the process of two processes; "industrialization creates supply and urbanization provides demand" to promote economic growth. During the period, the formation of debt is inevitable, but as long as the two-way progress smoothly, the cycle is long enough, and the debt can achieve a capital cycle.

But if this process is artificially accelerated, it will create huge structural contradictions at the economic and financial level. On the economic level, a large number of fixed assets and human capital are linked to specific industrialization stages, and are linked to infrastructure construction operations. Once the large-scale infrastructure construction process ends, or a new industrial revolution occurs, the contradiction of excess capacity in specific industries will be highlighted, and the economic growth rate may be sharp. decline. At the financial level, the assets corresponding to debt are mainly specific industrial equipment and infrastructure at a certain stage of development. When the two-way process enters the second half of the period, the demand will shrink sharply, which may lead to difficulties in debt service.

The above history has appeared in the economic history of Britain, the United States and Japan. Almost every technological revolution industrial revolution has made the economy that invested a lot of capital in the previous stage of industrial development face a transformational problem. If the formation of relevant capital is highly dependent on debt, it may trigger a financial crisis. Compared with developed economies, China's two-way process has been promoted more rapidly. In the same period, the degree of financial liberalization financial innovation is much higher than that of similar stages in Europe, America and Japan. Therefore, the contradictions reflected in the financial field are more concentrated and sharper.

Second, how serious the problem

After the international financial crisis, with the shrinking of external demand, domestic demand led by industrialized urbanization played an important role. Even so, it failed to curb the rapid decline of China's economic growth. In less than a decade, China's quarterly GDP growth rate fell from 14.4% in the peak of mid-2007 to less than 7%.

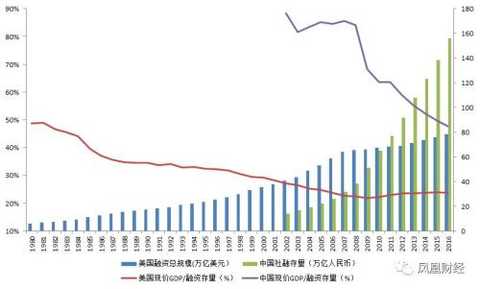

This period is also the golden age of China's financial sector development. Through various financial innovations and financial reforms, huge financial assets are allocated to the two fields. As a result of the rapid decline in economic growth and the rapid expansion of financing scale, the efficiency of China's financial output to the real economy has rapidly declined. From 2002 to 2008, the operating center of China's “current GDP output ratio per unit of stocks†was 0.85. After the financial crisis, the ratio fell rapidly, and by 2016 it had fallen to 0.48, a decrease of 0.37 from 2008.

In the early 1980s, the average GDP of the Americans was about 12,000 US dollars, and the ratio of the current GDP output of the unit stocks was 0.49, which is similar to the current situation in China. With the financial reforms in the 1980s and the development of financial markets, the proportion of direct financing such as the bond market has gradually increased, and the ratio has dropped back to 0.22 in 2009. Since the financial crisis, even with quantitative easing, the ratio operation center has basically stabilized at around 0.23.

Source: National Bureau of Statistics, Federal Reserve, US Securities Industry and Financial Markets Association, Bloomberg, Dongxing Securities Research Institute.

Explanation: The United States does not have the same social and financial statistics. We estimate the total size of the US social welfare = credit stock + bond stock % 2B stock market non-financial sector stock.

Among them, the credit stock: [US: credit market outstanding debt] - [United States: credit market outstanding debt: domestic financial sector] (Fed) (1945-present); bond stock: [United States: bond market outstanding amount : Total]-[US: Bond Market Unpaid Amount: National Debt] (US Securities Industry and Financial Market Association) (1980-present); Stock Market Non-financial Stock: [Deducting the IPO of the Financial Industry, Allotment, and Additional Issuance Financing] Bloomberg) (1900-present).

China and the United States have huge differences in GDP composition and financing structure. The horizontal comparison of data is lacking in meaning. However, since the financial crisis, the rapid decline in China’s ratio has undoubtedly been abnormal.

This may mean that the existing financial activities have Ponzi characteristics: the liabilities of financial activities are formed first, and the assets are formed later; the high output efficiency during the period of debt formation usually shows high financing costs, if the output efficiency is rapid in a short period of time If it falls, the assets that cannot find the corresponding rate of return in the current period match the previously formed liabilities.

But looking at the next decade, the situation may not be so pessimistic. The key is whether we have the ability to stabilize GDP growth, stabilize the size of debt, and prevent further rapid decline in financing output efficiency.

From the perspective of industrial supply, China's medium-level industrialization has been completed, and many industrial products rank first in the world. The total apparent consumption of some products has surpassed the historical peak, and some per capita consumption has exceeded the peak level of developed economies. There is little room for further expansion of the scope of assets and liabilities in the field. From the perspective of urbanization demand, in 2016, the urbanization rate of China's permanent residents was 57.4%. According to the current rate of urbanization rate of more than 1% per year, reaching the urbanization rate of about 70% in developed countries, it still takes about ten years. time. Looking at both ends of supply and demand, objectively there is the possibility of maintaining the efficiency of social financing output.

Third, ways to further ease the contradiction

The way to maintain the debt chain usually includes the following aspects: first, to maintain economic growth, to resolve conflicts through growth; second, to take various measures to control the size of debt in specific areas; third, to control financing costs through monetary policy and other technical means, and to promote debt extension . The de-capacity policy at the meso level also has a certain effect. The de-capacity policy so far has little effect on actual output, but it has a significant effect on improving the balance sheet of certain industries. The main risk facing the next step of the capacity policy is inflation. If the price increase in the upper and middle reaches eventually turns into comprehensive inflation, in theory, its effect is no different from debt monetization.

In addition, the policy to be considered in the prevention of debt risk is tax reduction. If a big debt crisis breaks out, the finances will certainly not be immune to it; instead of paying the bill after the crisis breaks out, it is better for the finances to intervene in advance to prevent problems before they happen. Tax cuts through the Laffer curve effect play a long-term positive effect on growth. Under the existing growth momentum pattern, if the tax cuts are reduced because of the reduction of infrastructure expenditures or the reduction of people's livelihood expenditures, it may lead to growth stalls in the short term. If the tax reduction policy is combined with the expansion of the deficit, it will be equivalent to the transfer of the debt burden from the private sector to the government sector, without reducing the total leverage of the whole society.

In order to maintain the deficit level and maintain the level of expenditure while reducing taxes, it is only the government departments to shrink. Governments at all levels in China manage the world's largest balance sheet. The total net assets of state-owned enterprises reached 44.7 trillion yuan in 2016, a year-on-year increase of 9.2%. Each year, the growth part is taken out and sold by means of mixed ownership reform. The corresponding income is used for tax reduction, which should be enough to block the debt gray rhinoceros.

The debt problem, the financial sector is playing "flowers", and ultimately the financial department must take out real money. This is in line with Ricardo's equivalent.

Cosplay Women'S Clothes,Cosplay Costumes Captain Marvel,Cosplay Costume Hela Anime,Cleopatra Anime Clothes

Shaoxing Jinshengtai Textile Co. Ltd , https://www.sxheptexs.com